العربية

العربية

Paying down your financial is almost certainly not as simple as you envision, yet not

Highlights:

- First-date family consumer funds are available to individuals that have never ordered a primary quarters. They might also be open to individuals exactly who satisfy particular other requirements.

- Finance one to aren’t appeal to very first-go out homeowners were bodies-backed FHA, Va and you will USDA money, and additionally down-payment direction apps.

- Also without being qualified to own regulators-backed loans or any other unique recommendations, first-date homebuyers can always get it done so you’re able to safer a reasonable mortgage with good conditions.

Buying your earliest domestic is going to be a pricey, nerve-wracking techniques. Luckily, newbie people is imagine numerous affordable funds. These types of finance are way more accessible to basic-go out people than you possibly might consider. They might even be a good idea having:

- Unmarried mothers which before simply had a house that have an old spouse.

- Anyone who has previously owned a property unfixed so you’re able to a permanent basis, instance a cellular or were created household.

- Individuals who possessed a property that has been maybe not doing strengthening requirements and could not be delivered to password for less than the amount it could cost to build another permanent construction.

It is installment loan Kansas possible to qualify for special financing, grants and other positives when you’re a low- or center- earnings buyer, when you find yourself a recently available or former armed forces provider affiliate or if perhaps you’re looking to shop for in a few geographical places.

The specific conditions one homebuyers must satisfy differ from financial to lender. So be sure to review the options carefully.

Sort of loans to possess very first-day homeowners

There are many form of money right for earliest-go out homeowners, even in the event down payment requirements or other terminology will vary. Many choices actually provide financial help.

Traditional mortgages

The definition of antique financial means any home mortgage it is not covered from the U.S. government and other groups. Consequently whether your borrower non-payments for the financing, the financial institution discover themselves baffled with the balance into the home loan.

Traditional funds have a tendency to bring all the way down rates and better full words than many other particular financial support. Yet not, these types of masters been at a cost: Given that antique finance perspective a high risk so you can lenders, they could be more complicated to help you qualify for and then have stricter credit criteria than other choices. It is really not impossible to own an initial-date homebuyer so you can be eligible for a conventional home loan, but authorities-supported finance should be far more available.

FHA loans

In the event your credit rating is under 620, you have got challenge protecting a normal financial. That’s where government-backed fund are in. Such as for example, FHA fund try backed by the fresh new Government Property Administration. Since your financial enjoys safety even if you’re incapable of repay your debts, FHA finance include a great deal more lenient borrowing from the bank requirements than of many old-fashioned financing.

FHA money generally want a credit score of at least 580 for recognition, provided you could invest in an effective step three.5% down-payment. Yet not, when you can pay for an excellent 10% deposit, you may qualify for an FHA home loan that have a credit rating as little as five-hundred.

Brand new downside to this entry to is the fact FHA financing need individuals to pay for individual home loan insurance policies (PMI). PMI superior help to reimburse the financial institution if your debtor defaults on the financing. PMI is commonly repaid about life of the mortgage and you may might possibly be determined given that a certain percentage of the base financing count.

Virtual assistant finance

The latest U.S. Institution regarding Veterans Activities (VA) provides access to loans to possess first-date homebuyers while some who happen to be effective-obligations military solution users, experts and you will thriving partners.

With this particular variety of loan, the Va partly promises mortgage loans off an exclusive bank. It means individuals found money which have better interest rates, all the way down closing costs, far more advantageous conditions and – oftentimes – zero downpayment. Va fund also are essentially exempt of high priced PMI. An important disadvantage to this type of loans is the fact eligibility is limited to help you consumers which have a connection to new military.

USDA money

The latest You.S. Institution away from Agriculture (USDA) even offers unique money getting lower- and middle- money outlying homebuyers employing Rural Creativity program.

When you yourself have an average money, you ily Property Protected Mortgage Program. Since this brand of loan emerges because of the a medication personal bank but backed by government entities, consumers normally found far more good conditions. If you’re a reduced-earnings debtor, you could qualify for a low-cost loan directly from the newest USDA, including short-term mortgage repayment assistance. Income qualifications for both programs may vary of the county.

USDA money are merely open to homeowners looking to buy an effective home from inside the select rural parts. You could make reference to the USDA’s eligibility map to find out more about qualifying cities.

Saving for a down-payment shall be prohibitively pricey for the majority first-big date homeowners. County and regional housing organizations render many DPA programs to help ease which weight for first-date homebuyers.

DPA apps feature varying terms, nonetheless they generally assist of the coating most of the otherwise the majority of your deposit and settlement costs. Certain, such DPA next mortgage loans, was repaid over time. Others, together with 0% interest deferred-percentage money, should be paid on condition that your refinance your mortgage otherwise offer your house. Some applications could even offer zero-strings-affixed DPA gives.

Certificates differ of the venue, Therefore check with your local homes company to see if you satisfy their requirements to own guidance.

Even if you don’t be eligible for DPA or any other unique guidelines, you could potentially however get it done so you’re able to safe a reasonable mortgage which have good conditions.

- Stay within your budget. Place a spending budget considering your revenue and you may stick with it through your family research. You shouldn’t be afraid in order to scale-down what you are shopping for, especially if you happen to be concerned with an expensive financial.

- Decrease your debt-to-income (DTI) proportion.Their DTI stands for the amount of financial obligation costs your debt every month split by your terrible month-to-month money. So it proportion is frequently referenced because of the loan providers since a measure of your capability to repay a loan. Lenders generally speaking offer mortgages into the most useful terms and you can reasonable appeal pricing so you’re able to individuals which have DTIs from thirty-six% or lower. To change your own DTI, you will need to both pay down your debt otherwise boost your monthly income.

- Rescue getting a bigger downpayment. Of numerous mortgage loans wanted a down payment of at least 20% of your own residence’s profit price. If you have higher credit scores, you really have specific flexibility in how far you really need to pay initial. However, lenders We in the event the downpayment try less than 20%, trying to strike that draw should be the easiest way to lower your general will cost you.

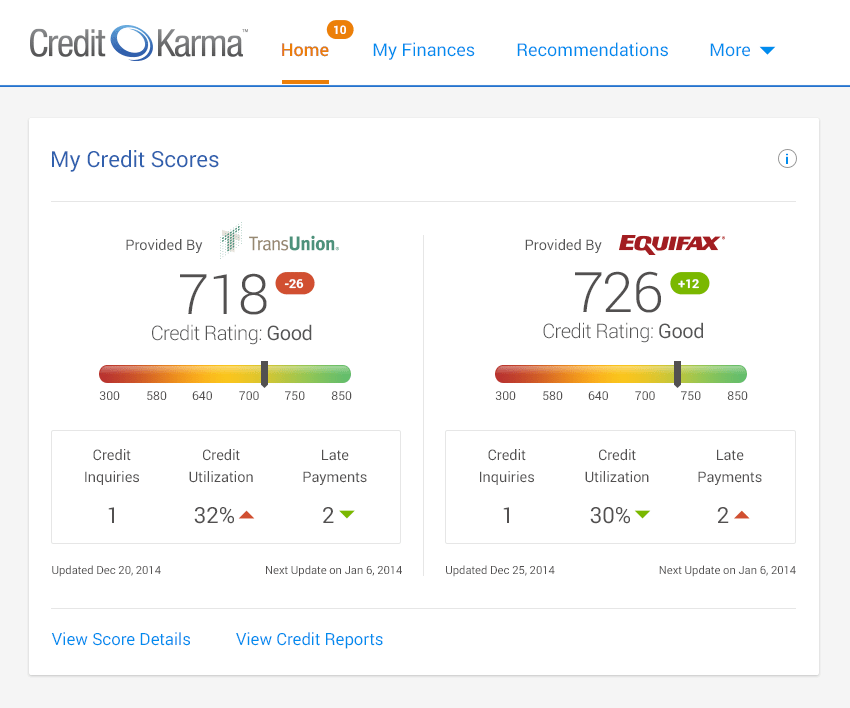

- Keep in mind your credit history and you may score. Lenders review your credit scores as one factor when evaluating the financial application, as well as to put their rate of interest and other loan words. The credit ratings or any other products, just like your earnings, may also impact the amount of money you be eligible for.

Sign up for a credit overseeing & Id theft security unit now!

Having $ monthly, you might discover what your location is that have the means to access their step 3-bureau credit report. Sign up for Equifax Done TM Largest now!

Voir aussi